The stickiness of Fossil Fuels

– what is slowing the transition to clean energy?

credit: pexels- ron lach

Oil Industry responsibilities for slowing transition

Al Gore in a recent article in Grist is quoted discussing the difficult of stopping climate change. After 40 years of campaigning on climate change from the first hearings he participated on the matter in the US Congress in 1981, he admits how surprised he has been that we have not been able to implement the kinds of policies that will solve the climate crisis. But the truth is if it were simply a matter of introducing policies and technologies to stop the release of greenhouse gases then the problem could and likely would have been solved years ago, particularly with the growing dire climate warnings and disasters as they become more frequent and deadly each passing month and year.

He squarely points the finger of blame at the fossil fuel industry which as ‘the most powerful and wealthiest business lobby in the history of the world… spare no effort and no expense to try to block any progress.’ This effort to first suppress and later minimise the impacts of burning fossil fuels has been well documented in a BBC series, Big Oil v the World which charted the stunningly successful efforts of US oil majors and their funded lobbyists to put the breaks on any effective action to stop the end of fossils fuels. As Gore states ‘they use their legacy networks of economic and political power to try to block any solutions of any sort that might reduce the consumption of fossil fuels.’

Understanding the actual advantages of fossil fuels to address those challenges

But if it was only a black and white story of the bad oil barons deceiving the rest of the world in pursuit of money and power then it is not likely that that cartoon would have lasted so long or have been so successful. Something else seems to be at play. It is a theme that Climate Junction will return to many times but simply put, it is not only a question of supply but also one, critically, of demand – people; businesses and states want to burn oil and gas and coal because of all its convenience and ease discussed in the Context articles on Coal, Oil and Gas (see the links at the bottom of this post) and the failure of the climate action lobby to fully take this on board, understand and deal with its reality has been an important weakness in the approach.

Cost is certainly a key factor in terms of demand for oil, gas and coal albeit the cost of alternative renewable energy sources for electricity generation have tumbled spectacularly in recent years. But where the speed of transition from fossil fuels is a critical factor understanding, the brakes and barriers to that transition are also essential. Certainly contending with the established infrastructure of fossil fuels (for pipelines and shipping, generation plants and centralised distribution networks as well as the petrol/gas stations for motor cars) as well as the energy density and availability of fossil fuels alongside the inertia of change where the last century has been built on oil, coal and gas are major factors. Compared with the intermittency issues, storage challenge (‘for when the sun doesnt shine and the wind doesnt blow’) , the material resources needed and the grid distribution challenges for renewables; the stickiness of fossil fuels is in fact not so surprising. Or rather it wouldn’t be if the climate crisis were ignored which it is a major tragedy of our time that it largely is or rather not being taken with the urgency that it demands. Nevertheless this longevity of fossil fuels should be understood in detail in order to help shift the curve in the shortest timeframe possible to prevent the worst impacts of climate warming.

What is slowing the transition to Renewablle Energy?

-Ability to meet demand

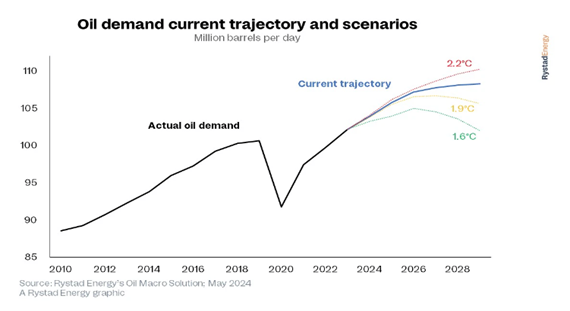

Looking at the industry journals may be a good place to start to consider the resilience in demand for fossil fuels ( if you accept that the reporting is inevitably slanted toward continued usage to be expected). Oil Price journal reported the analysis of Rystad Energy report on Oil Macro Scenarios that predicts an actual increase in oil demand in the medium term from two principal factors; first the actual and growing scale of demand for energy generally and secondly transportation.

Regarding the first; the report suggests the issue is that renewables are just not in a position to satisfy the increasing demand for energy either in terms of the rates of deployment or in its cost competitiveness. The article argues that ‘the process of substituting the capital stock associated with oil consumption will be complex, and lengthy due to the competitive advantages of oil in multiple transportation sectors and industrial processes’.

The report suggests that a fast transition away from oil will only be achieved if there are technical and economic breakthroughs in low-carbon energy carriers that can substitute for the advantages of oil. Essentially the rate of electrification of heating, industrial processes and transportation. This would necessitate the scaling of renewables to meet not only all new demand but can displace the existing infrastructures of the fossil fuels on cost as well as scale and that scale is enormous.

-Transportation

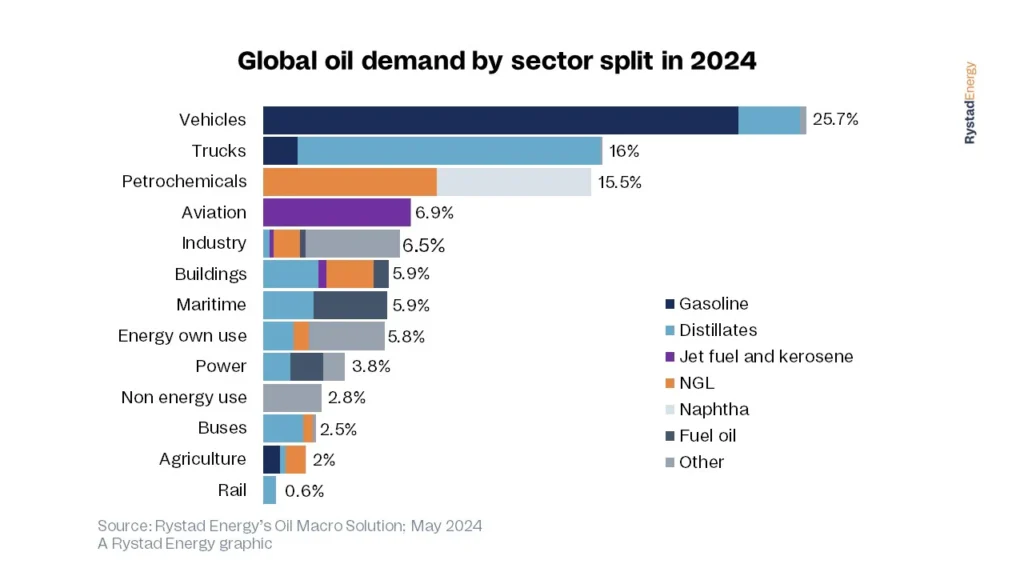

On transportation, the same report obviously highlights the key role of both electric vehicles; both battery (BEVs) and plugin hybrids (PHEVs) as key to the profile of oil demand as it accounts for a quarter of total global oil demand. Both the Rystad Report and the article point to the recent falling off of demand for EVs in last months related to vehicle range and charging fears as well as a cocktail of misinformation from action resistant sectors of the media.

Nevertheless the Rystad Report is actually optimistic for the return of demand for EVs in the second half of the decade driven by car manufacturer commitments and Government regulatory mandates in the EU and the UK though, the Oil Price article is doubtful about the technical capabilities of heavy goods transportation to transition due to battery limitations. Sustainable Aviation Fuel is also estimated to account for less than 5% of aircraft fuel by the end of the decade; and biofuel itself has substantial controversy related to its sustainability.

Other Sectors –

Other sectors called out as challenged by the transition are plastics which are estimated to soar with the globally expanding middle class and related consumption though the report does not address the major global efforts to reduce plastics usage. It sees oil and gas demand in the heating sector also more resilient than anticipated suggesting that heat pumps are not very effective in colder regions, although that will be news to Nordic users who lead the world in its usage!

In heavy industry, the report highlights the need for the high temperatures which fossil fuels provides readily supplies in furnaces whose essentials have been with us since the start of the Industrial Age when coal led the way. Hydrogen energy may be able to as well but clean hydrogen production is only at a very early stage and necessitates a large scale change in the cement, steel, aluminium and glass production processes which again involves substantial costs and time to transition, both of which would need to be factored in order to properly evaluate its potential.

However the article does not reference electric arc furnace technology for steel manufacturing which has the potential to substantially reduce the carbon emissions from which most new plants are deploying depending of course on the electricity source and is indeed being retrofitted at some plants such as at the Tata steel-works in the UK. The report and the article conclude on a positive point, noting how solar power is displacing coal over the past few years and concludes rather janus faced that ‘fast reduction in global emissions is still within reach, despite climbing oil demand.’ Having your cake and eating it, some might say but it is still a significant recognition for a fossil fuel trade journal. But it is not enough, we are in truth fast reaching a point where its either fossils or renewables; not both, certainly not increasing consumption of both for planet goals. Fossils may have a residual, peaking demand function whilst battery storage scales up but is only an issue of how long we can tolerate its continued usage as the severe impacts of climate change begin to mount across the world.

Conclusion –

The transition from fossil fuels may take take some time; embedded as the fossil fuels are in the economic infrastructure and social patterns of modern life and a reason for the general scepticism or reluctance of many to relating to the clean energy transformation. However and fundamentally, the analysis ignores the reason for the push towards clean energy; it is not really about cost benefits, security or convenience but connects to the fundamental survivability of the planets life systems in a fast heating world where the negative impacts are multiplying. It is the front and centre prioritisation of this core climate reality that provides not only a robust rationale for the transition but more importantly, at the point we have now reached in global heating, the speed of transition to a fully decarbonised energy system.

Although the Rystad energy report and the Oil Price article covering it are to varying degrees optimistic about the prospects for renewable expansion, they are both essentially take a gradualist, market and technology led transition approach. Ironically, this would probably have been a perfectly acceptable transition pathway if it had commenced back when in the 1990s when the first concerns as expressed in the early IPCC reports and UNFCCC climate change agreements were agreed. But as Al Gore keeps reminding us and the BBC series revealed in shocking detail, the transition was thrown off course by a sceptical public, cynically manipulated by the profit motives of big oil.

Now the most recent UNEP Emissions Gap Report , makes for depressing reading; indicating global average warming of 3 degrees centigrade on the cards, 2.6 degrees if all carbon reduction commitments were delivered in full (itself a stretch). This is principally due of course to the continuing increases in greenhouse gases from the inexorable growth of energy demand and the yet limited capacities of renewables to yet meet that demand; just as the Rystad report and Oil Price article highlighted. It is clear that business as usual even with massive increases in renewables in absolute terms factored in, it is still not enough and as the Gap Report shouts out, a step change is needed. As the Rystad report and article show, it may not be easy but it is possible and essential. Only question is are we ready and willing tomake the change?