Context – Sectors- BUILDINGS –

Content:

- Emissions and Energy Profile –

- Future Demand and Net Zero Targets –

- Emission Reductions – Potentials and Challenges –

- References

- Recent Posts and News Links

(Article Note – All references used in the Article are listed at the end of the article. Direct quotations are indicated in italics with emphasis highlighted in green.)

1.Emissions and Energy Profile –

Building Emissions and Energy – Percentages

Buildings are a major component in the transition to zero carbon emissions. In 2022 according to IEA building operations (excluding construction) accounted for 30% of global final energy consumption and 24% of global energy related emissions. The energy and related emissions is further divided into two parts: direct emissions from buildings which account for 8% of total emissions and indirect emissions, from the offsite electricity and heat used in buildings, which account for 16% of total global energy related emissions.

There is a third component of emissions which relates to the emissions created from construction in terms of the materials including the manufacturing and processing of cement, steel and aluminium for buildings which account, sometimes referred to as the ‘embodied emissions’ from new construction. According to IEA Embodied emissions from new construction account for 4% of final energy use and 5.8% of total energy related emissions.

Actual Emissions – Figures

Global buildings, direct emissions last reported by the IEA were 3 billion tonnes of CO2 or gigatonnes (Gt), this is a slight decrease ly in comparison to the previous 5 years when they were growing at approximately 1% per year.

Indirect building emissions reported are nearly 6.8 Gt CO2. This continues an ongoing trend related to the increasing use of electricity (electrification) in buildings and a total of 2.5Gt CO2 was altogether emitted in the construction related processes, ie “embodied CO”. Altogether building operations and construction emissions accounted for more than one third of total energy related emissions at 12.3Gt CO2. In the IEA World Energy Outlook 2024 (WEO2024) the IEA indicates that overall emissions in the building sector declined by 0.7% in 2023 but which it states were largely due to seasonal factors with a mild winter.

2. Future Demand and Net Zero Targets –

Buildings – Future Energy Demand

In the World Energy Outlook (WEO2024) the IEA estimates under its standard scenario, which is based on current global policies, the following (referred to as the Stated Policies Scenario – ‘STEPS’):

- Building sector energy growth overall continues to increase at a rate of 1% to 2030, broadly the same as present rates and then slows moderately to 0.7% from 2030 to 2050.

- Behind these figures are a number of cross factors some increasing consumption and others driving in opposite direction. The most significant being the divergence between developed and developing economies – in developed countries, energy consumption stays broadly static to 2030 and then starts to fall marginally at rate of 0.3% per year to 2050. Whilst for developing economies building related energy demand is estimated to grow by 1.5% to 2030 and then by 1.3% afterwards.

- Energy and related emissions growth in developing would be larger but for the anticipated switch from inefficient use of solid fuels to cleaner cooking and heating sources. Underlying these assumptions is the rate at which cleaner/more efficient sources of energy are adopted; a key one being heat pumps in place of gas heating and cooling, which will be looked at in further detail below as well as the source of electricity generation, the low carbon to fossil fuel mix.

Buildings Net Zero Targets –

The IEA has prepared a landmark Net Zero Roadmap Report outlining a detailed and viable pathway to zero carbon emissions by 2050 (NZ50), to keep within 1.5 degrees of warming, which has been taken as an authoritative benchmark for action across all sectors; first published in May 2021 and November 2024 in its current version as circumstances change and develop.

Rather than present its evaluation for ‘buildings’ as such, it presents its analysis of target energy consumption reduction for space heating and space cooling and energy efficiency respectively.

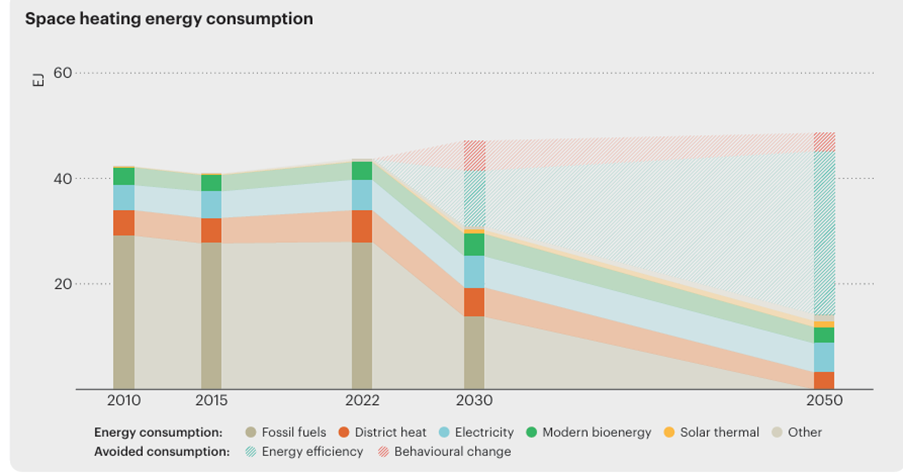

For space heating it indicates that energy consumption would need to fall by almost 70% by 2050 even with a 30% predicted increase in heated floor area. The reduction would come primarily from improvements in equipment efficiency and implementation of ‘zero-carbon-ready building energy codes. Following graph and tables presents the net zero pathway to 2050:

- A key aspect of the fall is the introduction of heat pumps which trebles in 8 years from 1000GW in 2022 to 3000GW in 2030 and continuing that steep increase to 4,400 by 2035.

- It also indicates that 100% of all new build are built zero-carbon-ready by 2030 with an extensive retrofit rate of 2.5% of all building stock annually to reach 35% in 2035 and 80% by 2050. While there is some evidence of this starting in the developed world, the developing world would struggle with the cost of such targets.

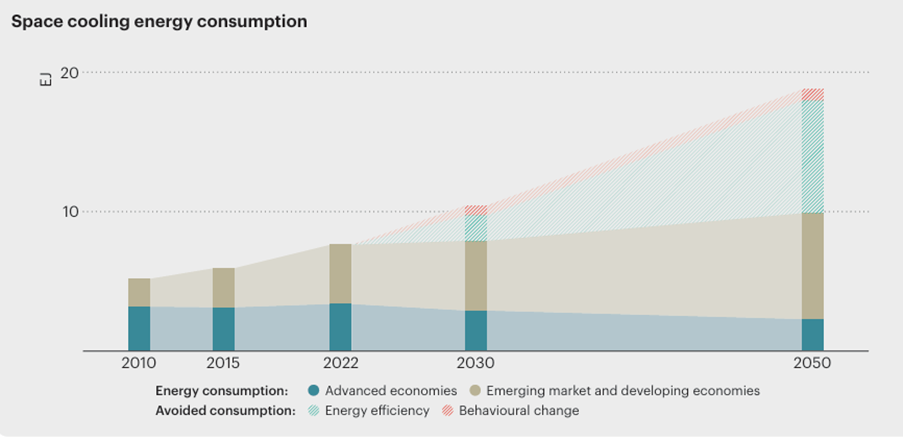

For Space Cooling, even with widespread use of designs features for natural cooling (‘passive designs’) and improvements in cooling equipment efficiency; energy consumption still more than doubles due to a heating climate and growing population and prosperity in the developing world. The growth without these measures would be much larger. Following graph and tables presents the net zero pathway to 2050:

- There is a sharp rise in the overall floor space cooling requirements from 105 billion square meters in 2022 to 170 billion square meters by 2035 and 250 billion square meters in 2050.

- Share of households with air conditioning goes from 36% in 2022 to 50% in 2035 and 60% by 2050 (which itself represents a significant moderation in growth rate assumption).

- Critically on these assumptions, average efficiency of new space cooling equipment in Watt-hour almost doubles to 2035 with more moderate improvement rates to 2050.

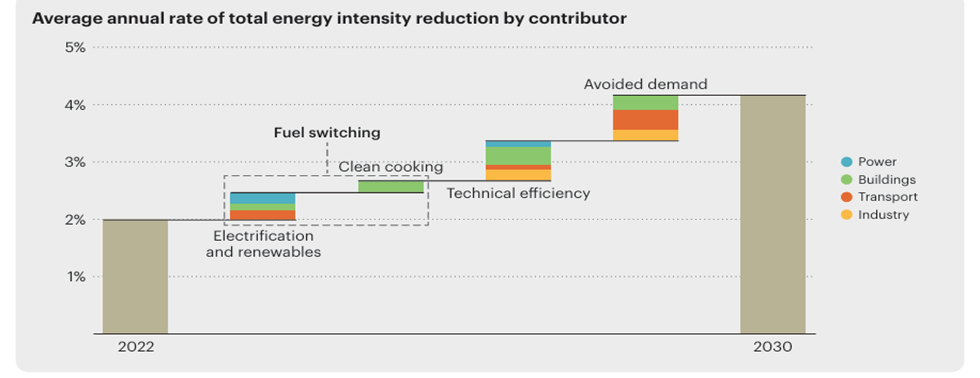

The analysis of Energy Efficiency, fuel switching and behaviour change is shared between power, transport, industry and buildings as fits this factor best.

Overall these measures would contribute a major 11% of cumulative emissions reduction to achieve the Net Zero 2050 target. Following graph and tables presents the net zero pathway to 2050:

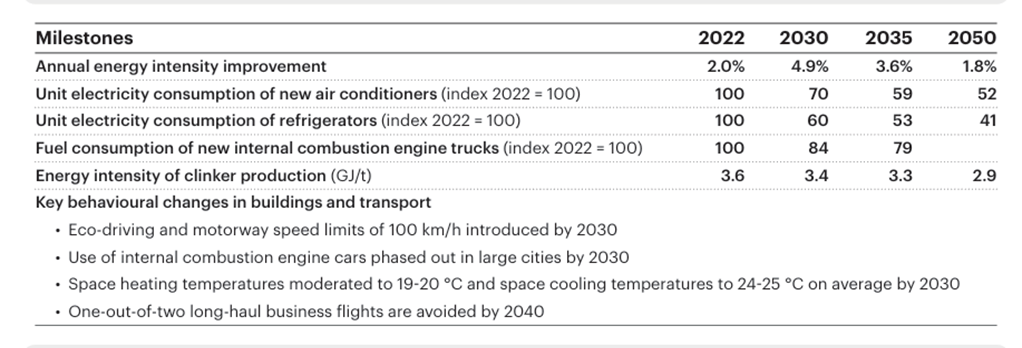

The key changes related to these factors are presented in the following table showing major improvements in energy intensity (more than doubling by 2030) and consumption for new air conditioning falling by 40% by 2030 and challenging behavioural moderation in the heating and cooling thermostat levels:

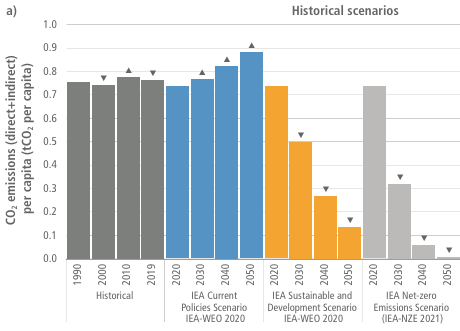

The IPCC’s 6th Assessment Report, Working Group 3: – Mitigation of Climate Change: (6thAR-WG3) in chapter 9 (Buildings) gives some indication of the change that these targets broadly represent in terms of change from current position related to residential buildings.

It indicates that global averaged emissions consumption attributable to buildings was 0.85tCO2 per person in 2019; by 2050 that would need to fall by almost exactly three quarters (75% reduction per capita) to 0.21tCO2 per person

The dark grey is historic, the navy is STEPS showing in broad terms no change (albeit that floor area more than doubles to 2050 so representing a reduction in absolute terms), but the mustard colour is the earlier version of the IEA Net Zero scenario from 2021.

It demonstrates the very steep falls on historic and current policy level consumption required to achieve the Net Zero Targets: a fall to 0.5tCO2 emissions by 2030 and continued reduction to 0.25tCO2 by 2030 which represent massive reductions on a global scale, even as we have seen that total floor area and cooling appliance use increases significantly. This raises the major question of how these reductions are achievable in the short time frames indicated with most of the heavy transition work being frontloaded in the next 10 years to 2035.

3. Emission Reductions – Potentials and Challenges –

Buildings Emission Reduction Potentials –

‘Sufficiency’–

The IPCC in 6thAR-WG3 related to buildings (c.9 of WG3 report), linked above, presents the term ‘SER’ standing for Sufficency, Efficiency and Renewables. ‘Efficiency’ referring to dong more with less in terms of efficiency of appliances, renewables references both the indirect source of energy coming from renewable sources as well as the direct generation of renewable energy in the home from solar panels for electricity as well as solar water heating.

What ‘Sufficiency’ refers to is the fair consumption of space bearing in mind the remaining carbon budget as the upper limit of usage and requirements for a decent living standards being the lower limits, achieved by avoiding demand or energy and materials reduction. As the report states at page 955:

‘Sufficiency interventions in buildings include the optimisation of the use of building, repurposing unused existing buildings, prioritising multi-family homes over single-family buildings, and adjusting the size of buildings to the evolving needs of households by downsizing dwellings. Sufficiency measures do not consume energy during the use phase of buildings.’

Basically sufficiency is minimising space usage to what is reasonable therefore avoiding new builds and maximising appropriate occupancy but within decent standards of accommodation. Two examples is the practice of ‘down-sizing’ once a family has grown and suitable tax and other measures to facilitate this or practice of suitably converting disused office blocks to living space and the appropriate planning permissions and conditions to allow this.

Another example in the business context is the increased use of ‘hot-desking’ where the total available desk space in office space is lower than the number of staff using that space. The final sentence stating that energy is not consumed during the use phase presumably means that the building is self sufficient in energy needs through a combination of high quality insulation (from cold and heat), combined with on-site renewable energy production from typically solar panels electricity with heat pumps etc.

High Mitigation potential–

The IPCC report indicates with ‘robust evidence, high agreement’ that that there is high carbon mitigation potentials in the building sector: up to 85% in Europe and North America and up to 40-80% in developing countries which aggregated reaches 8.2Gt CO2 and 61% of the baseline scenario which would go a long way towards the highly ambitious Net Zero goals.

The report also considers that this is achievable at reasonable low to no cost, presumably over the lifetime of usage as the up front capital costs can be significant but when the saved energy costs are factored over the lifetime of its use, the cost massively. The report states that high performance buildings will by 2050 be the standard at costs less than $20 tCO2 and in developing countries below $100 tCO2. The discrepancy between developed and developing country costs is not a type error but seems counter intuitive; but the significantly higher costs for developing countries must be a real concern in terms of the feasibility of implementation in those countries least able to pay. It could be an idea to see how carbon crediting could be extended to the building sector to help with the large scale of high performance development required in the developing world. Retrofitting existing buildings is much more expensive than new building efficiency measures with those measures for retro-fitting exceeding $200tCO2.

Renewable Energy, and Heat Pumps–

As considered in the Net Zero section above, heat pumps and cooling technologies will play critical roles in the building contribution to a sustainable world, along with renewable energy sourcing for supply of electricity in ongoing electrification trend. Renewable energy is considered in a separate Context Article but just to briefly indicate here that a key overarching strategy in the Net Zero pathway is the electrification of energy including in the building context the switch from gas boilers to heat pumps. This along with the anticipated significant growth in air conditioning needs (AC) will significantly increase the demand for electricity for the building sector as is already happening.

So it matters how that electricity is generated and the ability of renewables to meet the growing demand (as it is to date) as well as progressively taking the share of fossil fuel generation. Added to this is the growth in off grid renewable energy generation in both the developed and developing world.

Flexibility of supply will also be a key factor as much of domestic electricity need is of a peaking nature (ie. used in peak times particularly in the evening when people are at home especially in Winter months) so that would also need to be factored into the planning.

Air Conditioning–

In terms of cooling, the demand for space cooling has according to the IEA WEO 2024 has since 2000 grown more than any other sub-sector, increasing at an average of 4% per year, year on year. This is most pronounced in developing countries which will account for 75% of future projected growth, particularly from China and India and ownership levels will rise in developing countries from 0.6 per household to to close to 1.0 per household in ten years approximately to 2035 in line with current levels in the developed world. While under current policies this growth in demand is partly mitigated by efficiency due to important minimum performance standards although upfront (but not lifetime costs) is an important factor.

Heat Pumps–

Heat Pumps are in fact a form of energy switching, typically from fossil gas combustion to utilisation of earth or air heat sources with electric pumps. The WEO 2024 indicates that today heat pumps account for 12% of sales of residential heating equipment worldwide which is larger than what people might have thought and in France and USA sales have overtaken fossil fuel heating systems. That figure is expected to double in the next ten years under stated policies to 24% (STEPS) but are required under the Net Zero scenario to reach 40% by 2035.

However in 2023, sales actually fell 3% after two years of double digit growth except in China where sales rose by 12% bucking the trend. The increased growth in prior years was probably related to the price spiking for gas following the start of the war in Ukraine. The question is whether the sales can reach the target increase for the Net Zero Scenario or indeed for under the standard STEPS scenario. The potential barriers will be briefly considered in the relevant section below.

Efficiency Schemes, Building Codes and Appliance Performance Standards–

Allied to improvements in the efficiency of air cooling appliances and indeed space heating is the need to improve the insulation of the building itself, the building envelope. The IEA WEO 2024 reports (p117) on the Buildings Breakthrough initiative in which 27 countries, including 15 from the developing world, have committed to make nearly zero-energy homes and resilient buildings the norm by 2030. 70 countries have separately signed the Chaillot Declaration aiming to improve new building and materials efficiency.

Related to such schemes are the important issue of mandatory building codes related to heating systems and stringent performance standards for air conditioners. The challenge here, as will be looked briefly below will be public acceptance of stringent building codes, and the avoidance of performance standards and lax enforcement. Nevertheless they are considered to be essential tools in the transition to sustainable building development.

Other Benefits and Adaptation Measures–

The IPCC 6th Assessment Report stresses that these mitigation actions go far beyond the direct goal of climate action and encompass health gains through improved air quality. This is particularly the case from moving from solid fuel cooking to other forms reducing air particulates and general indoor air quality from improved heating, ventilation and cooling systems. In any general roll out of the measures it is essential that these immediate and direct benefits are emphasise.

Finally, as we move into a changed climate with more frequent, longer and more intense heatwaves as well humidity sea level rising and flooding the issue of adaptability particularly of new buildings is important. The IPCC highlights natural ventilation, white walls and green roofs as sufficiency measures which which are effective and decrease the demand for cooling. Similarly flood proofing or making buildings more resilient to extreme climate through building codes is another key consideration to future proof buildings.

Buildings Emission Reduction Challenges

Following are some challenges identified in the literature on building:

Heat Pumps: as the WEO indicates the upfront costs remain high, particularly for middle and low income families and particularly when to be effective it must be accompanied by good heat insulation measures. With declining cost of gas after the initial price shock following the start of the Ukraine war, it makes the heat pumps proposition less attractive.

There has been a backlash as well against stringent building code rules for instance in Germany where the there has been concerted misinformation campaign against installation impacting take up. Points to the need to engage clearly and honestly with the public on the costs and benefits.

There is also the issue of skilled installers shortages which is an issue in the UK as it is a specialist function which if not undertaken correctly, significantly reduces their effectiveness and/or efficiency.

Air Conditioners: While the issue with heat pumps is that the rate of installations may too low and slow, the opposite is the case with AC units. With the increased prevalence of extreme temperatures and extended heatwaves over much of India and China in 2024, there is a possibility of greater demand and longer usage times. This combination increases the peak electricity demand that puts pressure on the grid system as well as renewable energy storage systems which drives up fossil fuel generating systems.

As has recently been reported, although renewables supplied a record 40% of power in 2024, emissions continued to rise due to the increased demand for electricity and the need for more fossil fuel generation to meet the demand which is directly connected with a a significant increased demand for air coolers. If this is a continuing trend it could put in jeopardy the IEA Net Zero emission reduction aspirations for buildings.

4. Reference Links

World Energy Outlook 2024 – Analysis – IEA

Buildings – Energy System – IEA

IPCC 6TH Assessment Report – Working Group III: Mitigation of Climate Change Chapter 9: Buildings

Net Zero Roadmap: A Global Pathway to Keep the 1.5 °C Goal in Reach – Analysis – IEA

5. Recent Posts and News Items

Climate Junction –

Recent News Links –

- Heat pumps, EVs and net zero: What does the German election result mean for climate action? | Euronews – February 2025